How to Quit Your Job and Become a Freelancer

If quitting your job and becoming a freelancer was a simple as putting in your two weeks notice and setting up a home office, then this would make for a very short article.

While those may be the practical steps to get started as a freelancer, this article focuses on how to successfully become a freelance worker, hopefully making more than you currently make as an employee, and enjoying life much more as well!

Sound too good to be true? It isn’t. There’s a reason why so many people are self-employed and loving it. Even if you don’t make more than you did as an employee, perhaps you’ll find that your expenses are less (or you may have just cut back in order to have more freedom).

Whatever your circumstances may be, these tips for quitting your job and becoming a freelancer come both from my own experience, and those of others that I have met or learned from.

Let’s dive in!

Short on time? Download the cheat sheet.

Short on time? Download the cheat sheet.

First Off, Think Logically

Transitioning from employee to freelancer can be an emotional journey. You may be asking yourself:

- Am I ready to give up the stability of my paychecks?

- How can I give up my employee benefits?

- What if this doesn’t work out?

These are valid questions, let’s look at them one-by-one.

Your Job Wasn’t Stable Anyway

Okay, maybe with a union or some form of tenure you did have a pretty stable job. However, for most of us who are considering freelancing, our jobs really aren’t that stable. Companies downsize all of the time, their needs may change, or you may accidentally mess up and get fired! It happens, and it happens in a quick moment.

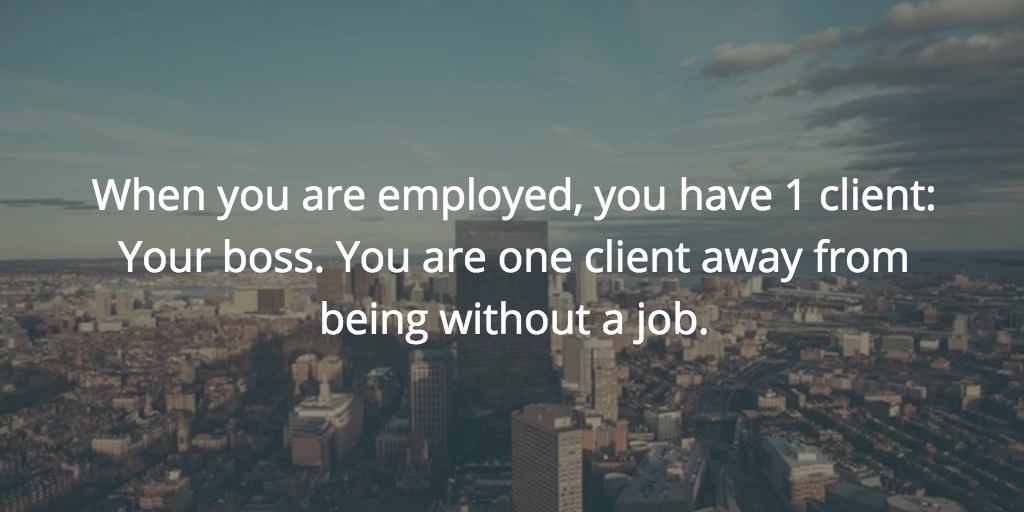

When you are employed, you have 1 client: Your boss. You are one client away from being without a job.

In contrast, as a freelancer I am often juggling multiple projects at different phases, and have a pipeline of new work coming in. If something goes awry with one project, I’ve got many others to fall back on.

The key to this stability is to ensure that you have a steady stream of freelance work coming in.

Employee Benefits are Just Money in Disguise

If you are thinking that there is no way you could give up the employee benefits that you currently enjoy with your employer, you’re absolutely WRONG.

There is a way…you just have to make enough money to cover these extra perks. According to some smart people at MIT, the typical benefits package for an employee with a $50,000 base salary breaks down as follows:

- $150: Life Insurance

- $2,000-$7,200: Health Insurance

- $250: Long-term disability

- $240-$650: Dental plans

In general, a salaried employee costs the employer 1.25 to 1.4 times their base salary. If a salaried employee leaves their $50,000/year job and ends up making $90,000/year as a freelancer, they can more than cover these extra benefits.

Of course, this is easier said than done, and it will take hard work to get to this level. What is crucial, however, is to realize that benefits are just money in disguise. So yes, there is a way to give up the benefits you currently enjoy…plan for them accordingly and charge what you need to cover them.

Need some inspiration that you CAN do this? Head over to the benefits page at Freelancers Union to find several insurance options for freelancers offered in your area.

Take Stock of What You Need to Cover

In the last section, I wanted to drive home the fact that you can provide similar benefits to yourself that an employer has been providing. However, I don’t want to paint an overly-rosy picture of what it takes to make it as a freelancer. Before taking the plunge, it is wise to have a plan to cover your financial needs.

This starts with taking stock of your financial outflow.

If you have access to your previous couple of month’s bank statements, this process is a lot easier. Just about every bank and credit card allows you to go online and print your past statements if you don’t have them available.

Fixed Expenses

This is easiest done with a spreadsheet, but you can also do it with simply a piece of paper a calculator. In one column, write down all of your recurring, fixed expenses. This might include your:

- Mortgage or rent

- Car payments

- Auto insurance

- Home or renter’s insurance

- Cell phone bill

- Internet

- Cable

- Giving/Tithing

- Bank fees

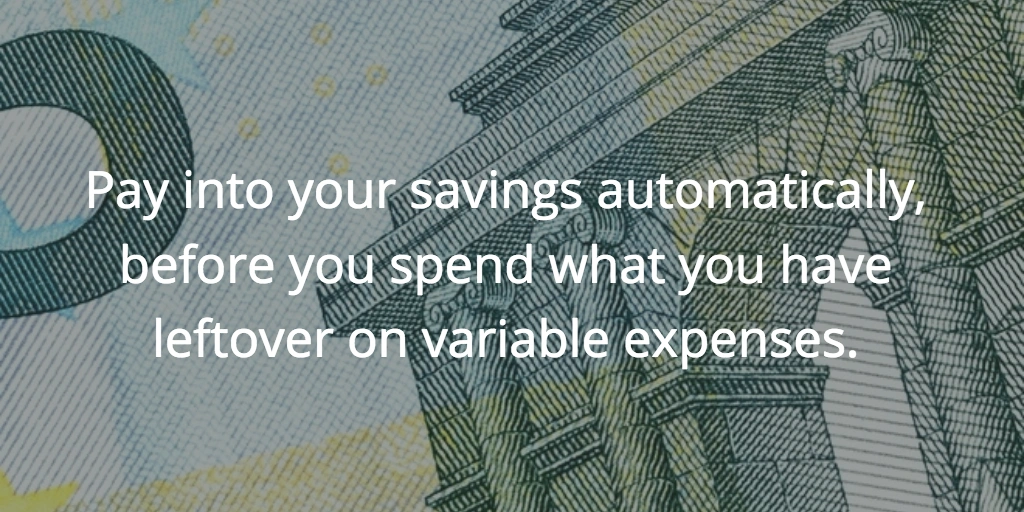

There is one more fixed expense that I like to add to the above, which most people treat as a variable expense, but I’ve found more success making it fixed and automatic…your savings.

You may have heard the mantra, ”Pay yourself first”, which basically means, “Treat your savings account like you do a mortgage". Pay it, automatically, before you spend what you have leftover on variable expenses.

You can set up a savings account through your bank, or even better, set up a money market account through a site like Vanguard. You can configure automatic withdrawals to come through every month without any action on your part after setting them up.

The advantage of a company like Vanguard is that you have access to other investment options once your savings fund starts to grow. Eventually, it will make sense to move some of that money into stock and bond funds for compounded growth over time.

If it sounds daunting to take this step, don’t listen to that fear. Start by setting up an automatic withdrawal for $20 a month. Just get into the habit. If you notice your bank account is starting to grow, then increase this monthly amount. I am constantly adjusting the amount I automatically withdrawal based off of the surplus or lack thereof in my monthly income.

Variable Expenses

After paying your fixed expenses, then it's time to list out your variable expenses. These are categories you typically spend money on in different amounts from month-to-month. You have the freedom to take from one category in order to splurge on another. Examples are:

- Food

- Transportation

- Clothing

- Entertainment

- Kids

- Gifts

- Household items

Your bank statements and a calculator will show you how much you typically spend in these categories. Another option is to sign up for Mint.com, tie in your accounts, and have these categories estimated automatically.

If you are taking the plunge into freelancing, these are the categories that you can usually cut back on in order to make the finances work.

Emergency Fund

If financial gurus recommend having an emergency fund of several months income when you are employed, imagine how much more important this becomes as a freelancer. You will have ups and downs in your income, so plan accordingly.

”Your freelance income can come in spurts and dry up for periods without much warning," -Anna Bassham, communications manager at Guru.com

Don’t splurge when you land that big project and the downpayment check comes in. Play it smart, save as much of that money as you can for the times when there are no new checks to cash.

Employee Benefits

Finally, you’ll need to budget in those benefits to cover what you will be giving up from your employer. Earlier in the article we mentioned the basic rule is to multiply your salaried income by 0.25 to 0.40 in order to determine what you might need to match your current benefits.

If you are fortunate enough to be married to someone who’s employer provides some of these benefits, then you’ll need a lot less to make it work. However, don’t neglect your own retirement. You’ll still want to set up a retirement account as a freelancer. In the US, some of your options are:

Again, Vanguard is a great resource for setting these up and managing them on your own. Of course, you could always talk to a financial advisor to help you out, but expect to pay 1-2% of your savings every year for their fees.

Get Full Buy-in From Your Spouse/Partner

If you’re married, your freelance career is going to have an impact on your spouse as well. They might have to work a little extra until your business takes off. They might have to watch the kids a little more or do more around the house because you are spending more time on your business.

Without their full support in your freelance switch, trouble is inevitable. Stress will creep in and have an effect on your relationship.

[My First Mistake] was not discussing my decision to quit my job with my husband. I knew he would talk me out of it. No, I turned in my resignation almost two weeks before letting my husband know that I had quit. Bad idea. -Teressa Campbell

You want your spouse in your corner. You have enough adversity to overcome by running your own business, it helps to have someone else in your corner cheering you on and helping out.

Think Differently About Your Rates

Knowing how much you’ll need to earn to make this switch to freelancing work, now it’s time to think about minimum viable rates that you’ll need to charge. I say minimal here because if you can go above and beyond that rate then all the better for you! However, you need to know what the minimum is, or else your just delaying the realization that this won’t be feasible.

Let’s say you need to make $70,000 in order to survive as a freelancer (and keep your current living standard). You’ll probably work around 40 hours a week, 50 weeks out of the year.

Do the math, and $70,000 / 50 weeks / 40 hours = $35/hr.

Stop. Right. There.

First of all, if you actually bill out 40 hours a week, that means you’re spending at least another 20 on acquiring new customers, billing current customers, keeping your skills fresh, and all of the other “non-billable” activities a freelancer finds themselves in throughout the week.

For simplicity’s sake, let’s assume you are only going to be billing for 20 hours a week. That means you’ll need to double that rate to $70/hr just to cover expenses.

Now let’s look at the second assumption in the above equation…you’re a freelancer now, are you really only going to take 2 weeks off all year?

Again, to keep it simple, let’s just bump up your hourly rate to $100/hr in order to cover your insurance, retirement, non-billable activities, and equipment (oh yeah, you’ll have to provide all of that stuff too).

You may be thinking, “no employer is going to pay me $100/hour!”

First of all, you’re thinking like an employee there. Remember, an employer knows that an employee costs them more money in benefits, so they are happy to pay a little more for a contractor that they don’t have to hire. In addition, they don’t have to spend time training you, or worrying about firing you when they don’t need you anymore or if it doesn’t work out:

“So charge them for your uncanny ability to turn on-off with the flip of your time tracker’s timer. Your rate should reflect the fact that you’re drastically easier to hire and fire than your employed counterparts.” -Brennan Dunn

Don’t be timid when it comes to setting your rates, remember that there are plenty of other freelancers out there charging even more than that.

Begin the Prep Work

Now that you’ve determined your rates, and sized up what it is going to take to make things sustainable as a freelancer, it is time to get your ducks in a row before making the final plunge.

It may be difficult to begin accepting clients and working as a freelancer while you are still employed, but some auxiliary business tasks can be handled before making the leap from employee to freelance worker.

Setup Your Business Structure

There are a number of loopholes to jump through once you start making freelance income. Depending upon how much you make, you will likely want to set up your business as a Limited Liability Company, or an S Corporation. What’s the difference between the two? Here’s come the fun part...

Talk to an Accountant

Even if you talk with an accountant and they recommend setting yourself up as a Limited Liability Company with pass-through income (meaning you file your taxes as an individual/couple with misc. income), at least you’ve established a relationship and ran your idea past someone who knows a little more about this than you.

After you start making a certain amount of money from freelancing, your accountant may advise you to file as an S corporation, which provides some added tax benefits while increasing the paperwork and costs needed. In the end, they will advise you whether or not it is worth it to go that route.

Talk to a Lawyer

Another person you want on your team as a freelancer is a lawyer, who can help you discover any potential legal hurdles you’ll have to jump through in your business. They can also be helpful in setting up your base contracts with clients, which can have some unique clauses based on your business type.

Even if you only have one meeting with your lawyer, establishing that relationship is a wise investment.

Talk to a Banker

After you’ve chosen a business structure and filed the appropriate paperwork, now it’s time to get that bank account!

This step is pretty easy, just walk into your local bank and let them know that you’d like to open a business banking account. They’ll walk you through it, give you some starter checks, and provide you with a debit card. This is key because once someone writes you a check to “YourBusiness, LLC”, you now have an account to deposit it into.

A separate bank account for your freelance business is also a wise move since all income and expenses can flow through it, greatly simplifying your accounting. In order to pay yourself, just write yourself a check from that account as a record.

Talk to Your Friends

Freelancer and advisor Emil Lamprecht writes:

The very first thing I did when deciding to make the switch was to get in touch with every single person I have ever known and told them my decision. I told them the field I was going to be working in and as it became clear, even the date I was planning to leave my awful day job (in 30 days time). -Emil Lamprecht

Your friends and acquaintances may very well be the connections to your first clients as a freelancer. Even if they are not in your target market, they are likely to know someone who is. Letting everyone know before you leave your job gives them some time to keep an eye out for someone in their network who might need your services.

Configure an Invoicing Tool

If you want to hit the ground running as a freelancer, you’ll want to become familiar with a time-tracking and invoicing tool like Harpoon, which provides a framework for tracking your expenses, time, goals, and getting paid by your clients.

Harpoon also handles automatic payment reminders, recurring invoices, and recurring expenses, to automate essential aspects of running your freelance business.

Final Step: Line up a Client

Finding clients can be the hardest part of freelancing, and something that you don’t want to take lightly when it comes to leaving your job and embarking on this new journey.

If you are debating quitting your job and you have confidence and skills (but no clients) then hold off on quitting your job. This may seem obvious to people who have already started producing money from their side-gig or side-biz, but newbies tend to under-estimate how long getting clients can take. -Anna Long-Stokes, Business Strategist

And don’t just assume that your employer will be your first client:

I know it sounds tempting to make your current employer your first freelance client, but it’s also important to find a few other clients before you walk into your boss’s office and announce you’re quitting your job to become a freelancer. -Nicole Dieker, Freelance Writer

If you know that you need to give your employer 30 days notice, then tell your first client that your current availability is 30 days from now. I once heard of an agency that intentionally booked their first clients 3 months out in order to create a sense of high-demand.

Telling a potential client that you are available right now can actually be a turnoff as they may wonder why nobody else is booking you. Use this to your advantage and tell book your first client as soon as possible, but state your availability in the future as to give your boss a proper notice when you quit.

Enjoyed these tips? Download the PDF Cheat Sheet Here for future reference.